Your favorite products might cost the same as they did one year ago, but there’s a good chance you’re getting a smaller amount. This is commonly referred to as “shrinkflation” or “downsizing,” one way consumers are affected by inflation. Inflation erodes the purchasing power of a dollar so that a dollar doesn’t buy as much as it used to. While inflation is different than changes in supply and demand in specific markets, like the recent surge in egg prices, it feels the same to consumers.

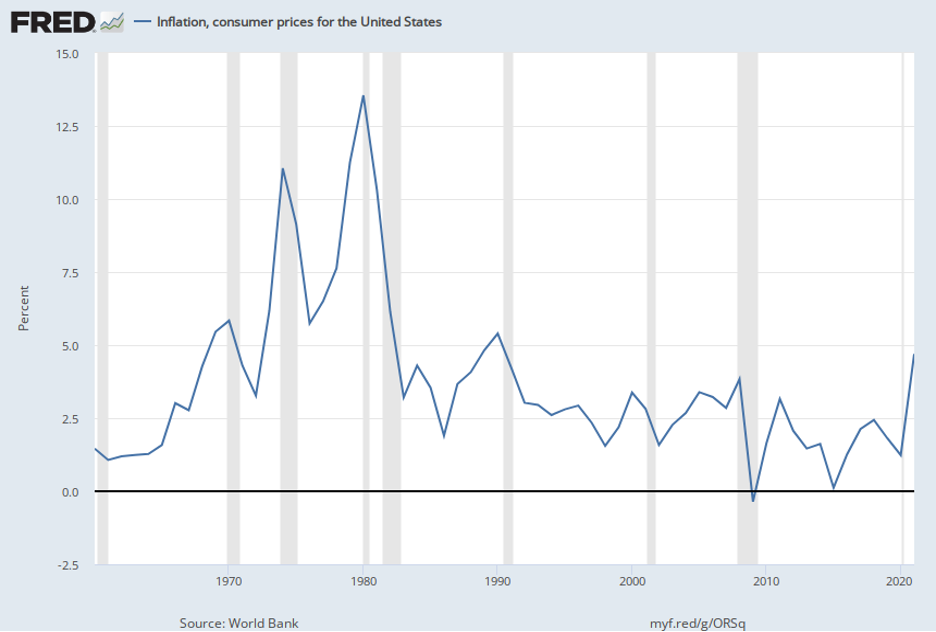

Inflation around 2% over the long-term is considered a healthy target. Short-term fluctuations, like we are currently experiencing, are common. The real damage from inflation to an economy comes from persistent inflation over many years. Inflation in the US has averaged 2.3% year-over-year between 1991 and 2019 and exceeded 5% only four times.

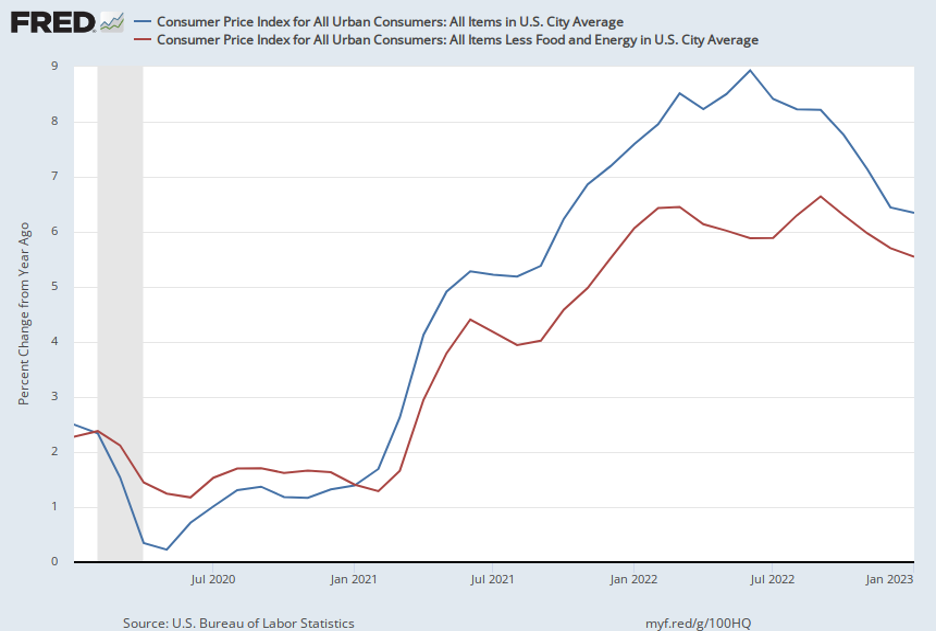

Figure 1 shows inflation at its highest in the 1970s and the effects of the Federal Reserve’s aggressive interest rate hikes to bring down inflation. While inflation in the US quadrupled in 2022, it appears the recent interest rate hikes are bringing down inflation though not as rapidly as consumers would like. The Fed’s challenge is to balance the need for low, stable inflation without overcorrecting and sending the economy into recession.

What You Can Do to Protect Yourself and Others

Basic personal finance becomes more important in times of uncertainty and inflation. So does taking care of ourselves through healthy sleep, movement, and nutrition because we make our best decisions when we are not in overstressed states arising from feelings of scarcity or fear.

- Prioritize an emergency fund. Only 50% of Mississippians report setting aside money for unexpected expenses, compared to 58% of the U.S. Set up regular savings to go directly into an account that is different from your checking account. Decide on an amount that you can live with for now, even if it is $10 per paycheck. Use the fund for real emergencies and pay the account back over time when you need to spend out of it.

- Find an account that pays a higher interest rate. The upside of higher interest rates is more can be made from saving. Mutual funds, Exchange-Traded Funds, online bank savings and money market mutual accounts, and 12-month Certificates of Deposit are paying 3-5% compared to 0.33% on savings accounts. Shop for higher interest accounts like you would for other products, including searching “best online savings accounts.” Always deal only with FDIC insured banks.

- Pay down credit cards aggressively. Do you know your credit card interest rate(s)? If you have multiple credit cards, pay attention to the different rates, and prioritize paying down the ones with higher rates. If you carry balances from month-to-month, focus on the APR, not the points or rewards which can distract consumers. If you can pay off the debt before the interest free period ends (e.g., 21 months), taking advantage of zero interest balance transfers can be a good move.

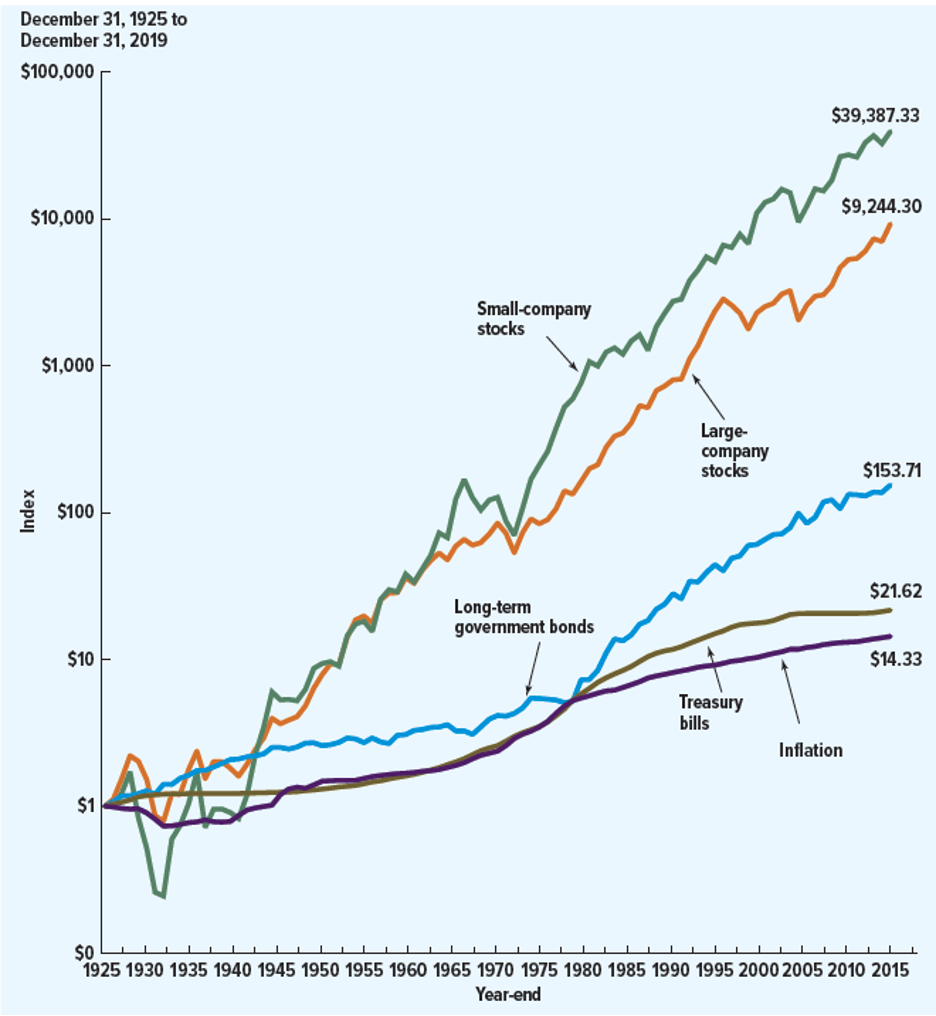

- Buy and hold. Investing in stocks, bonds, and Treasury bills is the best way to protect oneself from the effects of inflation in the long-term. The best strategy, regardless of how big the fluctuations can get, is to spread risk out by buying a “diversified portfolio” with many kinds of firms represented. For example, buying an “index fund” gives you a small fraction of each stock in that index. Many people get scared when they see the value of their stocks fall and wind up selling low. Reframe those stressful thoughts by remembering that when values fall, that can be a good time to buy more. Disregard the commercials selling gold and silver, their rate of return over the long run is barely above the rate of inflation. Use a “fee only” financial planner which can be found at https://www.napfa.org/.

- Consider strategies to curb spending. To decide if a product is worth the cost and get around persuasive marketing, take time to do the math to see how many hours of work it will take you to purchase the item. Use more generic items, , look for sales, and use coupons if it makes sense. Buying in bulk is a common strategy for lowering unit costs, but sometimes buying smaller units means a lower grocery bill and less waste because we don’t use all of what we bought in bulk. Be honest with family members about your values and goals around cutting expenses so they can get on board.

- Give to local food banks if you can. Household balance sheets got a reprieve with the COVID19 relief checks and people paid off debt and built saving. Those funds are dwindling and balance sheets for many are back to precarious pre-COVID19 levels and food insecurity is trending up. The most needed donations are cash and items like peanut butter, canned goods, and pasta, as well as personal hygiene products.

Rebecca “Becky” Smith, Ph.D. FFC © is an Associate Extension Professor in the Department of Agricultural Economics at Mississippi State University. She is the director of the MSU Extension Center for Economic Education and Financial Literacy and serves as the State Specialist Family Resource Management.

U.S. Bureau of Labor Statistics

“Shrinkflation” and its Impact on Inflation

More Americans are carrying debt, and many of them don’t know their APRs